Introduction

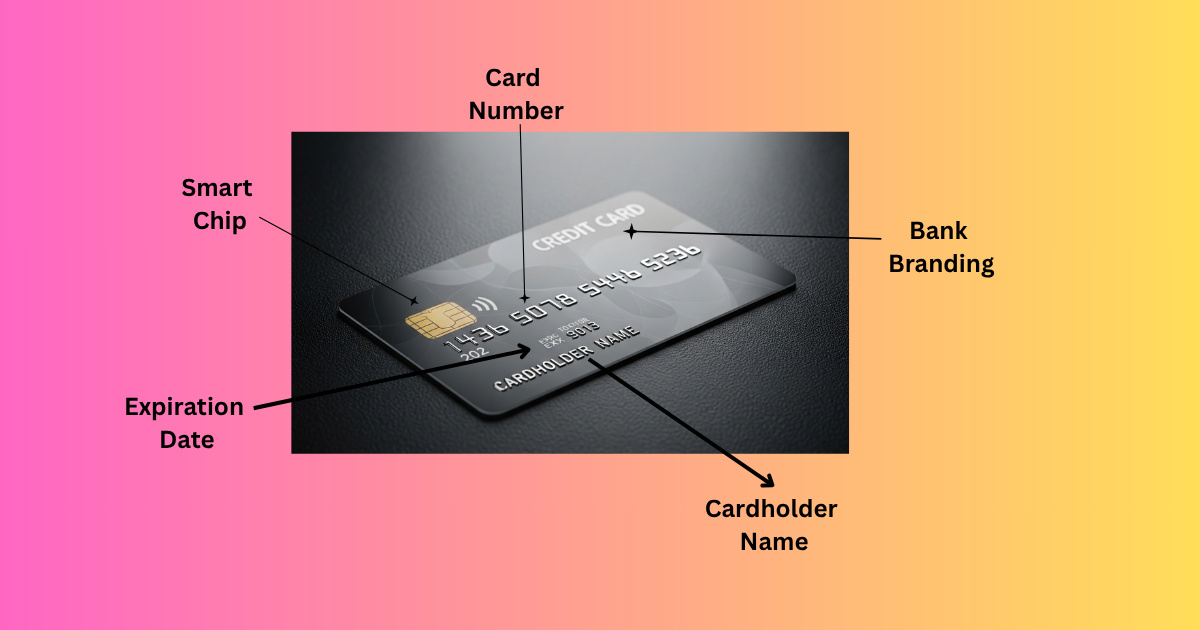

A credit card is a card issued by a bank or financial institution. Using this, you can pay for any product or service through borrowed money. You receive a bill every month in which you must return the money given to you—either with full payment or a minimum amount.Using a credit card wisely can lead to various benefits.When you use a credit card, you also have access to various benefits and rewards that can enhance your shopping experience.

Credit Card Benefits

- Cashless Transactions

You do not need to carry cash. You can make payments using the card anywhere, online or offline.

- Buy Now, Pay Later

Shop when you need it and pay later, as per your billing cycle.

- Rewards, Cashback & Discounts

You get reward points, cashback or special offers on every spend.

- How To Build Credit Card

Making timely payments improves your CIBIL score, which helps you in getting a loan in the future.

- EMI Facility

You can convert large slips into EMI easily without any extra documents.

- Fraud Protection

Understanding how to effectively manage your card can lead to significant savings over time.

If the card is lost or misused, the bank provides zero liability protection.

Credit Card Disadvantages

- High Interest Rate

If you do not pay the bill on time, you will have to pay high interest – up to 30% per annum.

- Debt Trap

Excessive expenditure and late payments can land you in a debt trap.

- Hidden Charges

Annual fee, Delayed fee, over limit charges

- Credit Score Down

If you do not make payments on time or use more than the limit, your score may get affected.

How to choose the best credit card?

1. Analyze your spending habits

- Do you shop a lot? Then get a cashback card.

- Do you travel? A travel rewards card would be best.

2. Fees Compare

Joining fee, annual fee and check missing payment.

3.Interest Rate

All credit card annual Percentage Rate check

4. Rewards & Offers

Evaluate potential rewards and benefits of different credit card options.

Choose cards that offer sign-up bonuses, milestone rewards or partner discounts.

Evaluating different credit card options based on your lifestyle can help you choose the best one.

5. Bank and App Support

Customer service and mobile app experience are also important.

Consider how much you use your credit card when choosing the right one.

Which Credit Card Is Best

🔝 Top Credit Cards in India (2025)

🛒 1. Best for Online Shopping

ICICI Credit Card

Understanding the terms of your credit card can help you avoid fees.

- Annual Fee: ₹0

- Benefits: 5% cashback for Prime users, 3% for others

- No expiry on reward points

- Works well on Amazon & partner sites

A credit card can be a valuable asset if used wisely, providing both flexibility and financial advantages.

🛍️ 2. Best for Lifestyle & Shopping

HDFC Credit Card

- Annual Fee: ₹1,000 (Waived on spend of ₹1L/year)

- 5% cashback on Amazon, Flipkart, Myntra

- 1% fuel surcharge waiver

- Free airport lounge access

✈️ 3. Best for Travel

SBI Card

- Annual Fee: ₹4,999

- Free Club Vistara & Trident Privilege membership

- Lounge access (domestic + international)

- Welcome voucher worth ₹5,000+

🧾 4. Best for Bill Payments & Daily Use

The Tata Neu HDFC Bank Credit Card can be very useful for monthly household expenses.

- Annual Fee: ₹499

- 5% cashback on bill payments (mobile, electricity etc.)

- 2% cashback on all other spends

- Very useful for monthly household expenses

✅ How to Choose the Best Credit Card for You:

- Where do you spend more? (Shopping, Travel, Groceries, etc.)

- Do you want to pay an annual fee or do you want zero fee?

- What is your monthly income?

- Do you want cashback or reward points?

How to Increase Credit Score: A Step-by-Step Guide

A good credit score is essential for getting loans, credit cards, and even renting a house. If your credit score is low, don’t worry — with a few smart steps, you can improve it over time.

What is a Credit Score?

A credit score is a three-digit number (usually between 300-900) that shows your creditworthiness. Higher the score, better your chances of getting approved for loans and credit cards at lower interest rates.

📈 Why Credit Score Matters?

- Easier loan approvals

- Lower interest rates

- Higher credit limits

- Better chances of renting homes

Tips to Increase Your Credit Score

1. Pay Your Bills On Time

Timely payments are the biggest factor in credit score calculation. Set reminders or auto-pay to avoid late payments.

2. Keep Credit Card Balances Low

Use only 30% or less of your credit limit. High usage signals risk and lowers your score.

3. Check Credit Report for Errors

Sometimes, wrong info can reduce your score. Check your credit report regularly and dispute errors.

4. Maintain Old Credit Accounts

Longer credit history = higher score. Don’t close old credit cards unless necessary.

5. Don’t Apply for Too Many Loans

Every loan application causes a “hard inquiry,” which can lower your score. Apply only when needed.

6. Diversify Your Credit Mix

Having different types of credit — like personal loans, credit cards, and EMIs — can improve your score if managed well.

Bonus Tools to Help You

- Use credit score checking apps like CIBIL, Experian, or CreditMantri

- Set payment reminders via SMS or email

- Use a secured credit card to rebuild credit

Conclusion

Building a strong credit score is like building trust — it takes time and discipline. Start by paying bills on time, keeping balances low, and being mindful of how you use credit. With patience, you’ll see your score rise and open doors to better financial opportunities.

How to Apply for a Credit Card:

Credit cards can make life easier — from managing expenses to building your credit score. But before applying, you must know the process, eligibility, and tips to choose the right card.

Step 1: Check Your Eligibility

Before applying, make sure you meet the basic requirements:

- Age: Usually 18+ (Some banks require 21+)

- Regular income (salary or business)

- Good credit score (usually 700+)

- Indian citizen or resident

Step 2: Compare Different Credit Cards

Choose a card based on your lifestyle and needs:

| Card Type | Best For |

|---|---|

| Cashback Cards | Daily spending |

| Rewards Cards | Travel, shopping |

| Fuel Cards | Petrol/diesel savings |

| Student Cards | Beginners, students |

| Secured Cards | Low credit score |

Use bank websites or comparison platforms like BankBazaar, PaisaBazaar, etc.

Step 3: Gather Required Documents

You’ll need:

- PAN Card

- Aadhaar Card / Address Proof

- Income Proof (Salary slip, ITR, or bank statement)

- Passport-size photo

Step 4: Apply Online or Offline

🔹 Online:

- Visit the official bank website or aggregator sites

- Choose the card and click “Apply Now”

- Fill in your personal & financial details

- Upload documents

- Submit the form

Offline:

- Visit the bank branch

- Fill out the form manually

- Submit documents and complete verification

Step 5: Verification & Approval

- The bank will verify your documents and credit profile

- You may get a call for confirmation

- If approved, card is dispatched within 7-10 days

Tips Before You Apply

- Check your credit score

- Don’t apply for too many cards at once

- Read all terms and charges (annual fee, interest rate)

- Start with a low-limit card if you’re a beginner

Best Credit Card for Students

Credit cards for students are a great way to build credit score, manage expenses, and learn financial responsibility — even without a full-time job.

What is a Student Credit Card?

A student credit card is specially designed for college/university students. It usually has:

- Low credit limit

- Minimal or zero annual fee

- No income proof required

- Easy eligibility

How to Get a Student Credit Card?

Option 1: Against Fixed Deposit (Secured Card)

Many banks offer a student credit card if you open a fixed deposit (usually ₹10,000+).

Option 2: Add-on Card (with Parents’ Card)

If your parents have a credit card, you can get an add-on/supplementary card.

Option 3: Through Student Account

Some banks offer credit cards if you have a student savings account with them (example: SBI Student Plus Advantage Card).

| Card Name | Key Features |

|---|---|

| SBI Student Plus Advantage | Against FD, fuel surcharge waiver |

| ICICI Bank Student Card | Against FD, reward points |

| Axis Bank Insta Easy Card | Instant approval, against FD |

| Kotak 811 #DreamDifferent Card | No income proof, against FD |

| HDFC ForexPlus Card (Prepaid) | Best for international students |

Documents Required

- College ID card

- PAN Card

- Aadhaar or Passport (as address proof)

- Fixed deposit (if applicable)

Tips for Students

- Use your card wisely – avoid overspending

- Pay your bills on time

- Don’t use more than 30% of your credit limit

- Track your spending regularly

Benefits of Student Credit Cards

✅ Build your credit history early

✅ Helpful during emergencies

✅ Safe cashless transactions

✅ Good for online subscriptions (like Netflix, Amazon)

Conclusion

A student credit card is not just about spending — it’s about learning financial discipline. Choose the right card based on your needs and build your financial future from day one.